Rohit had just received a 9% salary hike.

On paper, it looked impressive. His friends congratulated him. His family felt relieved. Even he thought, “This year will finally feel different.”

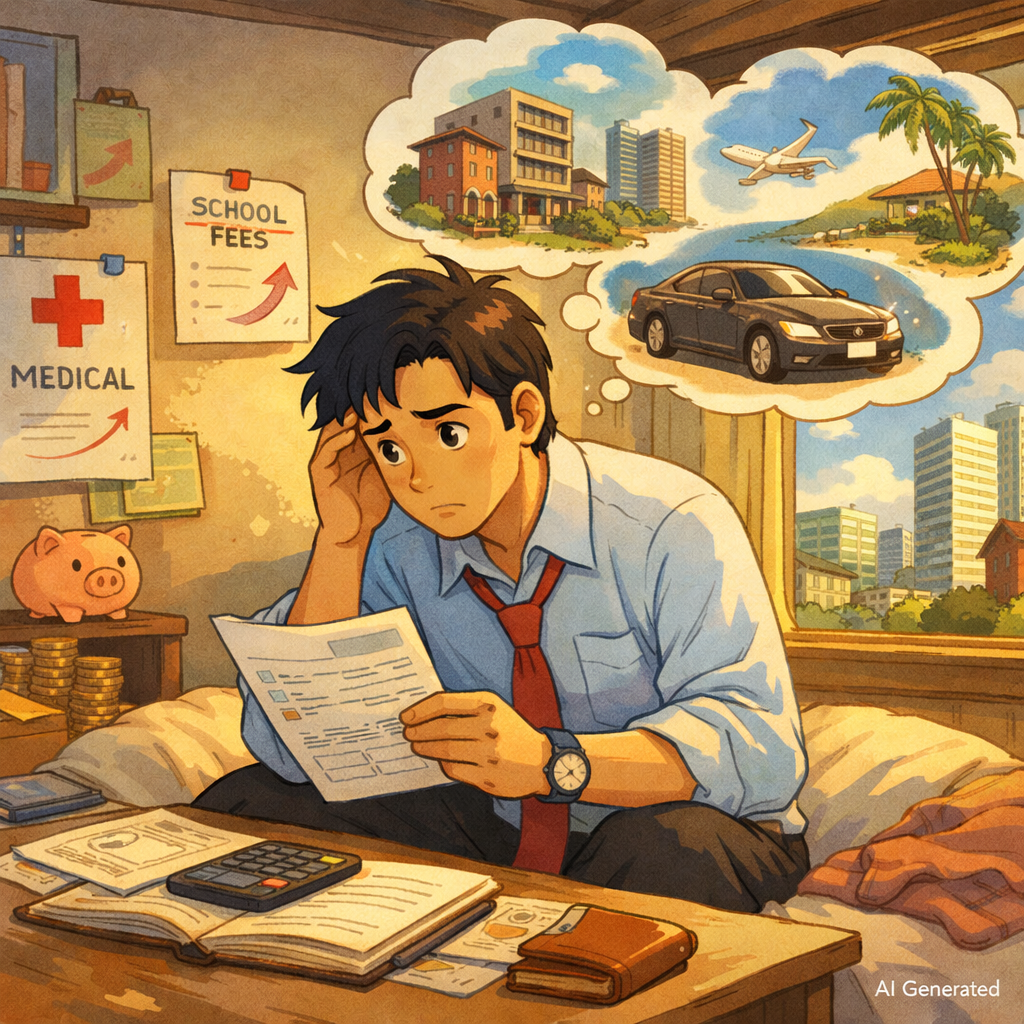

But three months later, something didn’t add up.

His bank balance wasn’t growing the way he expected.

In fact, it felt like nothing had really changed.

The Invisible Leak in Your Income

One Sunday morning, Rohit sat down with a cup of tea and opened his expense sheet.

- Rent had gone up again

- His child’s school fees had increased

- Health insurance premium had jumped

- Doctor visits were more expensive than last year

That’s when it hit him.

While his salary had increased by 9%, his actual cost of living had increased even faster.

This is what we call personal inflation — the inflation that actually impacts your life.

And for most urban families, it quietly runs ahead of salary hikes.

The Trap We Don’t Notice

Even if expenses weren’t rising so fast, something else was waiting.

After the hike, Rohit felt he deserved a better lifestyle.

So naturally, he started thinking:

- Maybe it’s time for a bigger house

- Maybe a car upgrade makes sense

- Maybe we can plan a more premium vacation

All reasonable thoughts.

But here’s the pattern: At first, every upgrade feels exciting. But within a few months… it feels normal.

The happiness fades.

The higher expense stays.

This is lifestyle creep — slow, silent, and powerful.

Why It’s Not About Discipline

Rohit blamed himself at first. “Maybe I just need to control my spending better.”

But the truth is — this isn’t just about discipline.

Three things are always working in the background:

- We adapt quickly – What feels like a luxury today becomes routine tomorrow

- Our surroundings influence us – As people around us upgrade, our expectations shift

- We reward ourselves – And honestly, after working hard, it feels deserved

So this isn’t a personal failure.

It’s a pattern almost everyone falls into.

The Turning Point

Then Rohit had a conversation with a friend who said something simple but powerful: “Don’t try to control your spending. Control what reaches your spending account.”

That one line changed everything.

What Rohit Did Differently

That year, Rohit’s salary increased by ₹10,000 per month.

Instead of letting the entire amount flow into his lifestyle, he made one rule:

- ₹5,000 → goes straight into investments

- ₹5,000 → he can spend freely

No guilt. No overthinking.

Why This Worked?

Two things happened:

- He still enjoyed the benefits of his raise

- But he also ensured that half of it started building his future

And because this was automated, there was no daily struggle of “Should I save or spend?”

The decision was already made.

The Real Power Shows Up Later

Over the years, Rohit kept repeating this habit.

Every time his salary increased, his investments increased too. And slowly, quietly, compounding started doing its job.

Years later, the gap between:

- Investing a fixed amount

vs - Increasing investments every year

…became huge.

Not because he earned dramatically more.

But because he structured his behavior better.

What Rohit Finally Understood

He realized something simple, yet powerful:

You don’t build wealth by controlling expenses every day.

You build wealth by deciding once — and automating it.

The next time your salary increases, pause for a moment and ask: “How much of this raise will actually stay with me? And how much will quietly disappear into a better lifestyle? “

Because if you don’t make that decision upfront…

Your lifestyle will make it for you.