Part 1 — The Big Picture

Shyam: Ram bhai, I’ve been hearing scary things — petrol prices rising, global tensions, gold going haywire. Should I be worried about my savings?

Ram: Shyam, you’re not alone. In the past few weeks alone, I’ve had dozens of investors sitting right where you are — panicking, questioning everything, and seriously considering moving all their money into fixed deposits or gold just to feel safe. The urge to run to safety is completely human. But before you make any move, let’s understand what’s actually happening — because reacting to noise without understanding it is often the most expensive mistake an investor can make.

Shyam: That’s exactly how I feel — like I just want to put everything somewhere safe and stop watching the numbers fall.

Ram: I hear you. But “safe” in the short term can quietly become “costly” in the long term. Let’s break it down step by step — once you understand what is happening and why, that fear starts to lose its grip.

Shyam: Please. Start from the beginning.

Ram: The root of most current worries is oil. Our country imports enormous amounts of crude oil. When tensions rise in oil-producing regions, global prices spike — and our import bill becomes very heavy very fast.

Shyam: But pump prices haven’t gone up yet. Isn’t that good?

Ram: Short term, yes. But someone is absorbing that extra cost — right now, it’s the government. They’re dipping into our national reserves — think of it as the country’s savings account — to cover the gap. That can’t go on indefinitely.

Shyam: So those reserves are shrinking?

Ram: Gradually, yes. These are called Forex Reserves — India’s emergency fund in foreign currency. They keep the Rupee stable and signal financial health to the world. With oil expensive and fuel prices unchanged, reserves are under pressure. The longer this continues, the more strain on the economy.

What are Forex Reserves? Our country’s foreign currency emergency fund — used to pay for imports like oil, gold, and electronics. When reserves fall, the Rupee weakens and imports get costlier, creating a ripple effect across the entire economy.

Part 2 — What Comes Next

Shyam: So what will the government do?

Ram: Eventually, they’ll likely raise petrol and diesel prices — passing the cost to consumers. Painful, but responsible. You simply cannot keep bleeding the national wallet. When that happens, inflation rises — fuel costs trickle into everything. Transporting vegetables, manufacturing goods, running businesses — all become costlier. Sectors like banking, housing, and automobiles slow down as people spend more carefully.

Shyam: What about gold? Why is the government asking people not to buy it?

Ram: Our country imports a massive amount of gold every year, all paid in foreign currency. Every gold purchase chips away at our reserves. Recently, import duties on gold were reduced significantly, which caused imports to surge. Now, to protect reserves, the government may raise those duties again — making gold costlier to import and slowing the drain.

Shyam: So gold stocks could fall further if duties go up?

Ram: Exactly. If duties rise, gold companies face pressure and stocks could drop more. If duties stay unchanged, the current dip is actually a buying opportunity in quality gold stocks. That duty announcement is the signal to watch.

Part 3 — The Stock Market

Shyam: My portfolio keeps falling. I keep hearing foreign investors are leaving the country. Is it that bad?

Ram: It’s real and significant. Foreign Institutional Investors — the big global funds — have been selling Indian stocks heavily. This is directly hurting your portfolio. But here’s the key — India hasn’t done anything wrong. It’s about global competition for money.

Shyam: What do you mean?

Ram: Think of it like two restaurants. Restaurant A offers solid, reliable food. Restaurant B just launched a dish everyone’s obsessed with and profits are extraordinary. Where does money flow first? Right now, the AI boom is Restaurant B — global investors are chasing extraordinary returns in markets with semiconductor and chip companies. Our country doesn’t have that story yet, so money flows there instead.

Shyam: Will foreign investors ever come back?

Ram: They will. Two triggers could bring them back fast — first, if the AI boom slows, funds seek the next opportunity and our country, with its strong growth projections, becomes very attractive. Second, any peace resolution in ongoing global conflicts. Markets reacted with sharp single-day gains just on ceasefire rumors — imagine a real, lasting peace deal.

The Silver Lining our country’s economic growth remains among the highest of any large economy globally. Foreign selling reflects competition for global capital — not a loss of faith in country’s fundamentals. The long-term story is very much alive.

Part 4 — What Should You Do?

Shyam: Enough about the problem. What do I actually do with my money?

Ram: Two answers — one for long-term investors, one for shorter-term moves.

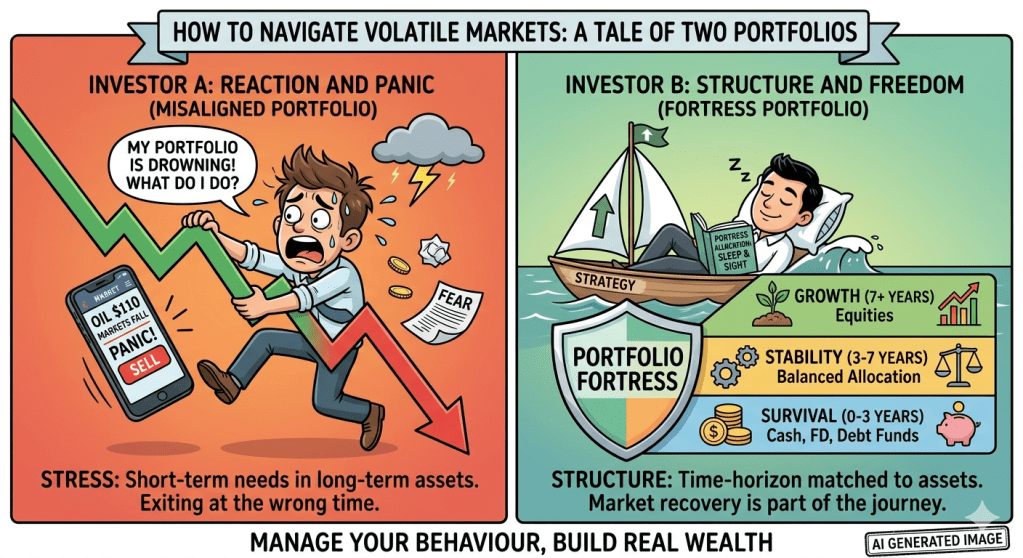

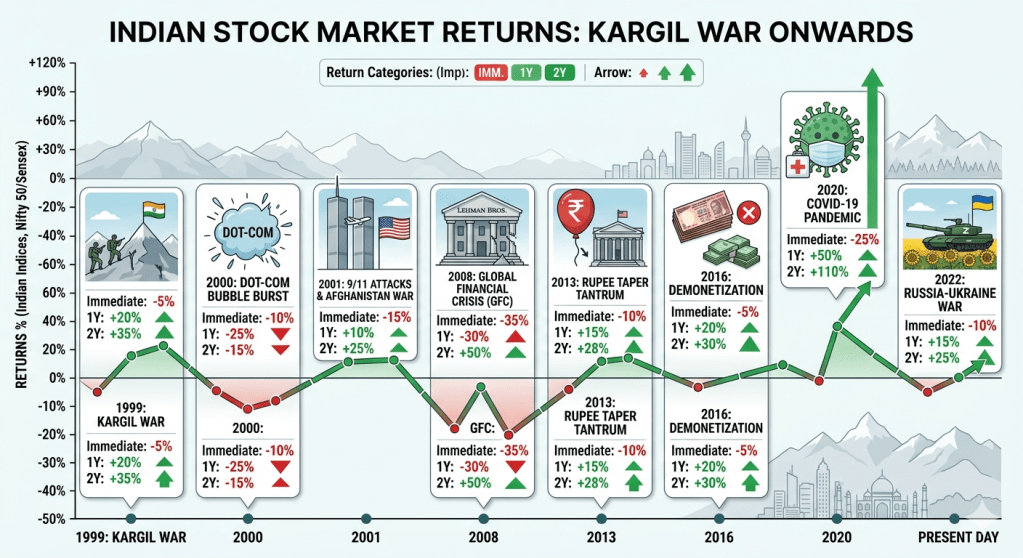

For the long term: your most powerful weapon is patience. Our country has survived wars, recessions, crises, and pandemics. Every time, markets recovered and reached new highs. The investors who stayed calm and didn’t sell at the bottom built real wealth. Markets don’t rise every year — some years are flat or negative — but when recovery comes, it comes fast and powerfully, wiping out all the quiet years at once. You cannot afford to be sitting in cash when that surge happens.

Shyam: What about my SIPs? The market keeps falling — feels like throwing money into a hole.

Ram: Do not stop your SIPs. When markets fall, your fixed monthly amount buys more units. When markets rise, those extra units multiply your gains. Stopping SIPs in a falling market is like walking out of a sale because prices are too low. It makes no financial sense whatsoever.

Shyam: What if I have extra money to invest now?

Ram: Don’t just chase price drops — focus on valuations. A stock that’s fallen 30% isn’t automatically cheap, and one that’s risen isn’t automatically expensive. Look at Price-to-Earnings (P/E) or Price-to-Book (P/B) ratios and compare them to their 5-year averages. If today’s valuation is well below that average, you’re likely getting a good deal. Banking stocks, for instance, are currently trading meaningfully below historical averages — interesting for a patient investor with a 1-2 year horizon. Real estate stocks have also corrected — enter in small portions, don’t go all-in, and hold patiently.

Shyam: One last thing — what’s your single biggest piece of advice for someone feeling nervous right now?

Ram: Don’t let fear make your financial decisions. Fear is a terrible investor. People waited for the market to fall — now it has fallen and they’re too scared to act. The market rewards courage and patience, not perfect timing. Stay in the game. Keep your SIPs running. Avoid panic selling. Look for value when valuations make sense. The country’s growth story is intact — this is a turbulent chapter, not the end of the book.

Shyam: I came in panicking and I’m leaving with a plan. Thank you, Ram bhai.

Ram: That’s all any of us need — clarity over panic. Remember: in investing, the best action during chaos is often disciplined inaction. Stay the course. You’ll thank yourself later.

⚠️ Disclaimer – The content in this article — is created purely for general awareness and educational purposes. It is not intended to be, and should not be construed as, financial advice, investment guidance, or a recommendation to buy, sell, or hold any asset, security, or financial instrument.

Before making any financial decision — whether it relates to stocks, mutual funds, gold, real estate, or any other asset class — I strongly urge you to consult a qualified and registered financial planner or investment advisor who can assess your personal goals, risk appetite, income, and circumstances.

This article does not establish a client-advisor relationship of any kind. The characters of Ram and Shyam are fictional and used solely as a storytelling device to simplify complex financial concepts for a general audience.

Invest wisely. Invest informed. Always seek professional guidance.