Siya: Ram, I have to be honest — I’ve been losing sleep over my portfolio. I keep hearing that the stock market has lost a massive amount of value. Is it really as bad as it sounds?

Ram: I understand the anxiety, Siya. The numbers are big, and they sound scary. The market has lost a very significant chunk of its total value compared to its all-time highs — we’re talking somewhere in the range of 17% to 20% of the country’s entire annual economic output, just gone from stock market valuations. So yes, it’s real. But before you panic, let’s talk about why this is happening, because that matters more than the number itself.

Siya: Okay. Everyone around me is saying it’s because of rising oil prices and global tensions. Is that true?

Ram: That’s the popular explanation, and it’s partly right. But here’s the thing — if oil prices were the only reason, then every country that imports most of its oil would be suffering similarly, right? And that’s not quite what we’re seeing. The deeper problem is something most people aren’t talking about: foreign investment flows.

Siya: Foreign investment? What do you mean exactly?

Ram: Let me give you a simple picture. A few years ago, foreign money was flowing into our markets in huge amounts — tens of billions of dollars ($) every year. That money was supporting company earnings, keeping the currency strong, and pushing the stock market higher. But over time, the gap between money coming in and money going out has been shrinking. And in the last couple of years, there’s been almost no net foreign investment left.

In fact, we’ve been losing more than we’re gaining.

Siya: So money is leaving the country?

Ram: Yes. On two fronts. First, large foreign investors who came in during the boom years are now taking their profits and moving to other opportunities — which is normal behaviour in a mature market, but it puts pressure on us. Second, our own companies are investing abroad in large amounts — tens of billions of dollars ($) — because certain other countries offer lower taxes and simpler regulations.

Siya: And this is affecting the rupee (₹) too? I noticed my international transactions feel more expensive lately.

Ram: Absolutely. This is one of the clearest signs of the problem. The rupee (₹) has been weakening — not just against the dollar ($), which you might expect, but also against the currencies of smaller neighbouring economies. That tells you it’s not just a global dollar ($) story. When foreign investment dries up, demand for the rupee (₹) falls, and it depreciates. It’s like the price of anything — if fewer people want it, it gets cheaper.

Siya: This is worrying. So what is being done about it?

Ram: Regulators are aware. There are efforts underway to make the market more accessible and investor-friendly — easing certain rules, conducting currency swap auctions to shore up foreign reserves. These are technical measures, but they signal that the issue is being taken seriously. The fix, though, isn’t overnight. Attracting investment back requires rebuilding confidence, improving the regulatory environment, and time.

Siya: While all this is going on, what should I be doing? I’m tempted to just pull everything out.

Ram: And that, Siya, is exactly the mistake I want to stop you from making. Let me tell you about the two biggest errors I see investors make in times like these.

Siya: Please, tell me.

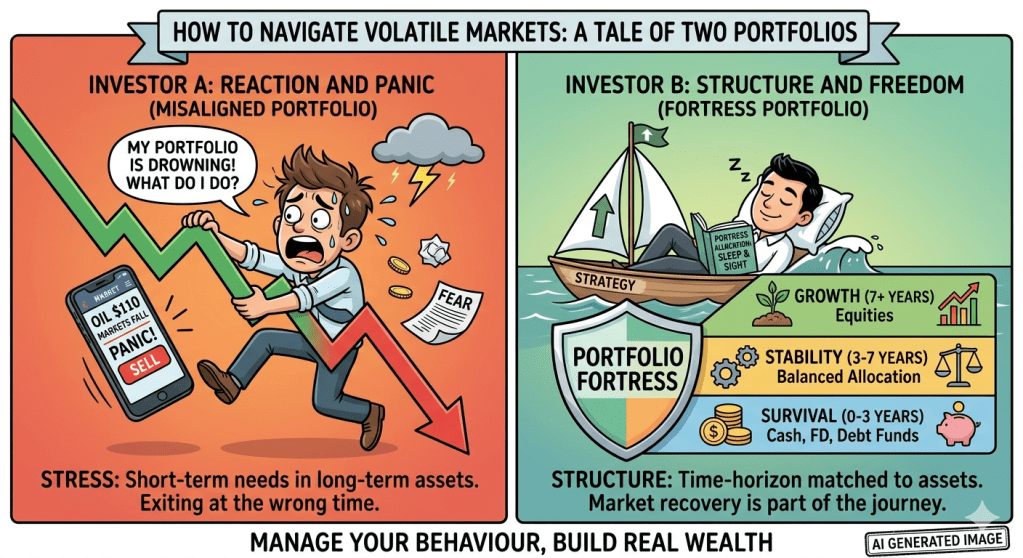

Ram: The first mistake is having no cushion.

Most investors put everything into market-linked investments — mutual funds, stocks, ETFs — and nothing in safe, fixed-return options. When markets fall, they have no stable ground to stand on, so panic sets in. A simple rule of thumb: keep at least 10 to 15% of your portfolio in something that gives you a fixed, predictable return, like a fixed deposit or a recurring deposit. If you’re retired or close to it, that number should be much higher — closer to 75 to 85% in stable instruments.

Siya: I never thought about it that way. I always assumed fixed deposits were “boring money.”

Ram: Boring money is the best money when everything else is burning! It’s your financial shock absorber. And if putting a large lump sum aside feels difficult, a recurring deposit works beautifully — you put in a small, fixed amount every month, it builds the habit, and your money earns decent interest safely. Look for options where you can compare rates across multiple banks, and make sure your deposits are insured up to the regulatory limit so your money is protected even if a bank has trouble.

Siya: That makes sense. What’s the second mistake?

Ram: Panic selling your mutual funds. This is the one that costs people the most, and I’ve seen it happen again and again. The market dips 20, 25, even 30%. Investors can’t take the pain of watching their portfolio bleed on screen, so they sell. And then — almost always — the market recovers. The people who sold have now locked in a permanent loss, while those who stayed have recovered, sometimes fully.

Siya: I’ll be honest, I did look at my mid-cap fund last month and almost hit the sell button. The NAV had dropped almost 25% from its peak.

Ram: I know. It feels like the right thing to do in the moment. But think about it this way — you didn’t “lose” that money until you actually sold. On paper, a drop is just a number. The real loss happens when you exit at the bottom and then watch the recovery happen without you.

Siya: So I should just… hold?

Ram: Not blindly. There’s a difference between panicking and reviewing. If your fund has strong fundamentals — good historical performance across market cycles, a solid management team, a clear investment strategy — staying invested is almost always the right call during short-term volatility. But if you were in a fund that was already underperforming even in good times, a downturn is a good moment to review and possibly switch — calmly and deliberately, not out of fear.

Siya: This has been really helpful, Ram. So to summarize what you’re telling me: the situation is real but not catastrophic, there are bigger forces at play beyond just oil prices, and my job as an investor is to stay diversified, stay calm, and not make decisions out of panic.

Ram: Perfectly put. The economy and the market go through cycles.

The investors who build wealth over time are not the ones who got lucky predicting every dip — they’re the ones who stayed disciplined when it was uncomfortable. Keep some money safe, keep your long-term investments intact, review but don’t react, and you’ll be fine.

Siya: Thank you, Ram. I’m going to go set up that recurring deposit today.

Ram: That’s the best thing I’ve heard all week. Small, steady steps — that’s how real financial security is built.

**Have questions about managing your portfolio through market volatility? Drop them in the comments below.