It was a usual Sunday morning.

Rohit, a mid-level professional and a disciplined SIP investor, sat with his cup of tea scrolling through the news.

“Markets fall sharply amid global tensions…”

“War fears shake investor confidence…”

“Experts warn of further downside…”

His heart skipped a beat. He opened his portfolio.

Red everywhere!!

Just last month, he was feeling confident. Today, fear had taken over.

The Emotional Trap

Rohit called his friend Amit. “I think I should stop my SIPs… maybe even sell some funds. What if markets fall more?”

Amit paused and asked one question: “Do you remember what happened during COVID in 2020?”

Rohit nodded.

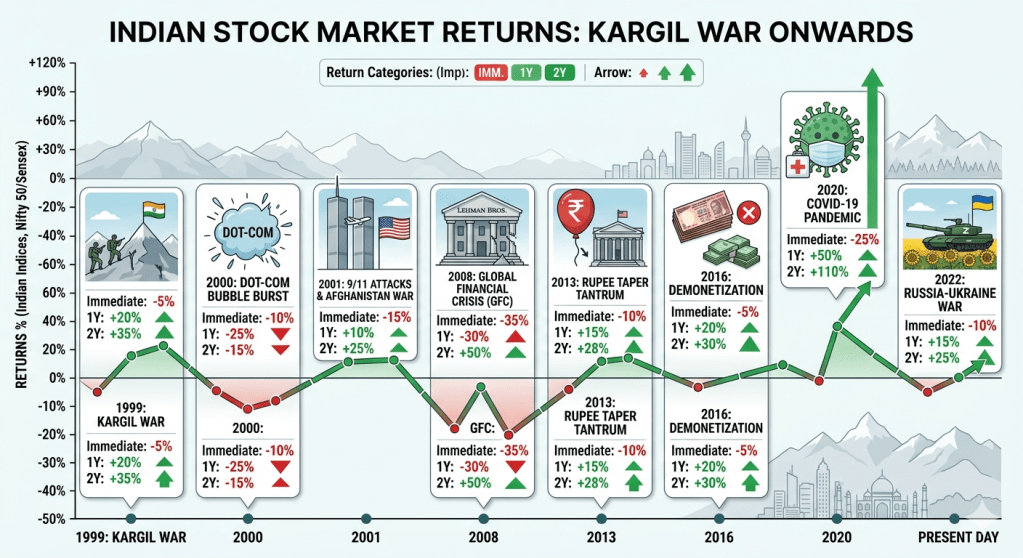

Markets had crashed 25% almost overnight.

But what happened next?

- Within 1 year: +50%

- Within 2 years: +110%

History Doesn’t Repeat, But It Rhymes

Amit continued: “Let’s go back further…”

- Kargil War (1999): Short-term fall, strong recovery

- Dot-com crash (2000): Painful, but temporary

- Global Financial Crisis (2008): Markets crashed ~35%… then doubled

- Demonetization (2016): Panic → Recovery

- COVID (2020): Fear → Massive rally

- Russia-Ukraine War (2022): Same story

Every single time:

👉 Markets fell sharply

👉 Investors panicked

👉 And then… markets recovered and moved higher

So What Separates Winners from Worriers?

Amit smiled and said: “It’s not about timing the market… it’s about time in the market.”

Let’s simplify this.

There are two types of investors:

1. Reaction-Based Investor (Rohit Today)

- Stops SIPs when markets fall

- Sells in fear

- Waits for “clarity”

- Misses recovery

2. Goal-Based Investor (Rohit Tomorrow)

- Invests with a purpose (retirement, kids, wealth)

- Ignores short-term noise

- Uses volatility to accumulate more

- Stays consistent

The Real Truth About Equity Markets

Equity is like the ocean

- Calm sometimes

- Stormy at times

- But always moving forward over the long term

Volatility is not a bug.

👉 It is the price you pay for higher returns

Why This Is the Time to Act (Not Panic)

When markets fall:

💡 You are buying the same businesses at lower prices

💡 Your SIP buys more units

💡 Future returns potential improves significantly

This is where the famous principle comes alive:

“Buy when others are fearful.”

Goal-Based Planning: Your Anchor in Chaos

Instead of asking: “Should I stop investing?”

Ask: “Has my financial goal changed?”

If your goals are intact:

- Your retirement is still 15 years away

- Your child’s education is still 10 years away

Then why react to a 3-month market fall?

The Turning Point

Rohit closed his app.

He didn’t stop his SIP.

In fact, He increased it slightly.

Because he finally understood: “This is not a crisis… this is an opportunity in disguise.”

Final Thought for You :

Markets will always test your patience before rewarding your discipline.

- Wars will happen

- Crashes will come

- Fear will spread

But…

- Wealth is created by those who stay invested

- And accelerated by those who invest more during fear

So what should be your Action Plan?

- Stay invested

- Continue SIPs

- Align with goals, not headlines

- Use dips to accumulate

- Trust the long-term journey