Ram and Shyam both joined Central Government service in 2004.

Same department. Same salary. Same promotions.

For years, their financial lives looked exactly the same.

One Evening Over Tea…

Shyam said: “I met a financial planner recently. He explained something interesting about NPS.”

Ram replied casually: “What more is there? Tier I is already getting deducted. That’s enough.”

Shyam smiled: “That’s what I thought too… but there’s a smarter way to use it.”

The Small Decision That Changed Everything

Ram’s Approach

- Continued with only NPS Tier I (mandatory)

- Extra savings went into FDs and traditional options

Shyam’s Approach (After Advice)

The planner told him: “Use Tier II as your growth engine. Just invest ₹5,000 per month and forget about it.”

Shyam followed:

- ₹5,000/month in Tier II

- Continued Tier I as usual

Fast Forward to 2026

After 22 years…

They meet again.

Ram Shares His Numbers

“I stayed safe. I didn’t take risks.”

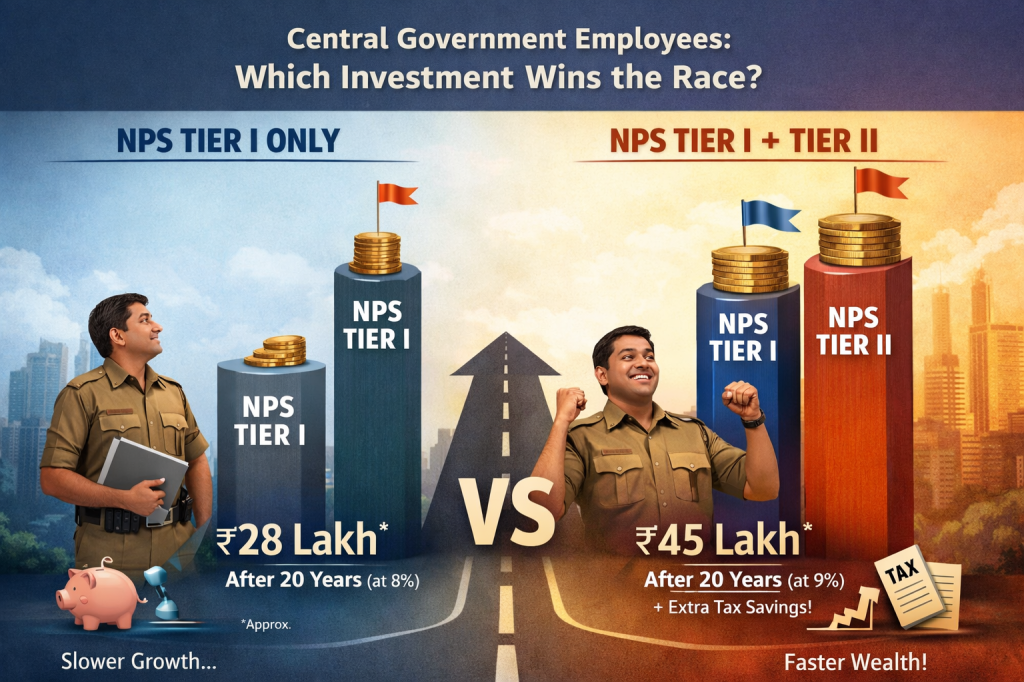

👉 His savings (mostly FD-based): ~₹26–28 lakh

Shyam Shares His Numbers

“I didn’t do anything complex. Just stayed consistent.”

👉 His Tier II corpus: ~₹36–38 lakh

Ram is Surprised

“We earned the same… how did you end up with more?”

Shyam replies: “I didn’t save more… I just used a better vehicle.”

The Real Game Begins Near Retirement

At age 58, Shyam meets his planner again.

Planner says: “Now use Tier II to save tax.”

Shyam’s 3-Year Strategy (Simple and Effective)

- Age 58 → Moves ₹50,000 from Tier II to Tier I → saves tax

- Age 59 → Moves ₹50,000 → saves tax

- Age 60 → Moves ₹50,000 → saves tax

Then Shyam Asks a Smart Question

“Why not move my entire ₹30 lakh into Tier I and save more tax?”

The Planner Explains the Reality

Tax benefit is LIMITED

Even if Shyam moves ₹10 lakh (or even ₹30 lakh):

👉 He cannot claim full tax deduction

Because:

- Only ₹50,000 per year is allowed under Section 80CCD(1B)

- Tax benefit applies only to Tier I contributions

Planner Simplifies It

“Tax rules don’t reward how much you invest…

they reward how well you use the limit.”

Why Moving Entire Corpus is NOT a Good Idea

The planner continues:

You lose liquidity

- Tier II → flexible

- Tier I → locked till retirement

No extra tax benefit

- Still capped at ₹50,000

More money gets locked into annuity

- 40% must go into pension (less flexibility)

What Ram Realises Late

Ram asks quietly: “I never used Tier II… can I still do this?”

Shyam replies: “You can… but you missed the compounding journey.”

The Simple Strategy Every Govt Employee Can Follow

During your career:

- Invest ₹3,000–₹10,000/month in Tier II

- Stay consistent

Near retirement:

- Move ₹50,000/year from Tier II → Tier I

- Claim tax deduction

Final Conversation

As they walk out on their last working day…

Ram says: “We earned the same… but you planned better.”

Shyam smiles: “I didn’t plan better… I just started one small step early and used it wisely.”

Final Takeaway

👉 Tier I is your foundation

👉 Tier II is your advantage

And most importantly:

👉 Don’t move everything… move only what gives you tax benefit