Rimmi: Gyan, guess what? I finally bought my dream mobile phone — on Zero Cost EMI! !

Rimmi:No interest, no extra charges. Feels like a total win.

Gyan: Ah, the sweet illusion of “free.” You’re not wrong, but also… not entirely right.No interest, no extra charges. Feels like a total win

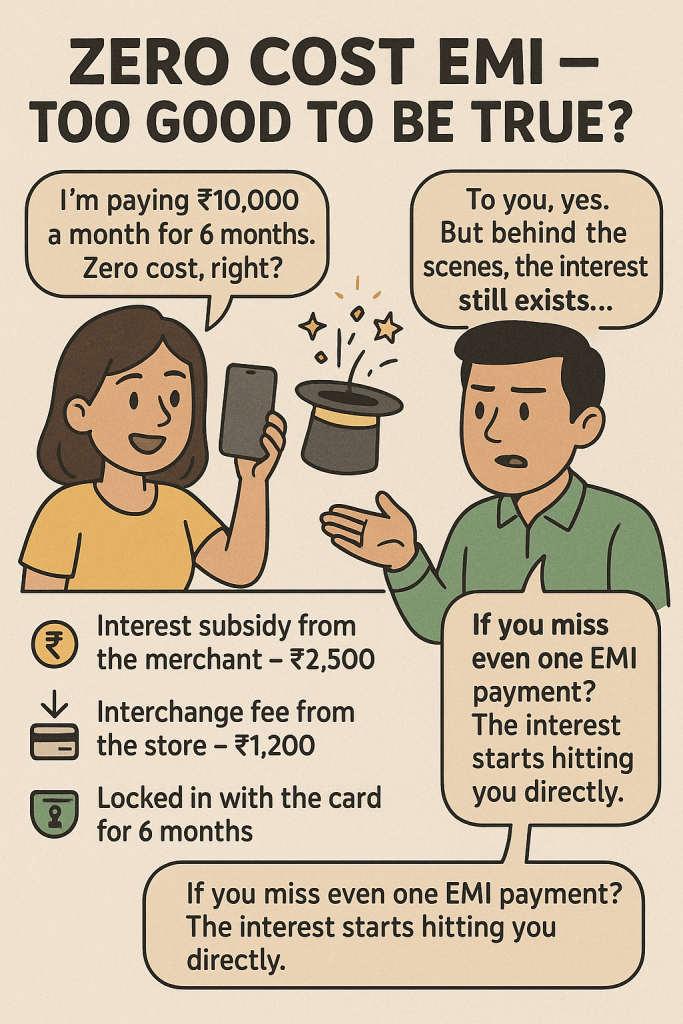

Rimmi: Wait, what do you mean? I’m paying ₹10,000 a month for 6 months. That’s the exact price — ₹60,000. Zero cost, right?

Gyan: To you, yes. But behind the scenes, it’s like a magic trick. The interest still exists — it’s just being paid by someone else.

Rimmi: So… who’s footing the bill? The mobile company?

Gyan: Could be a mobile company. Could be the store. Whoever is desperate to make the sale. Think of it this way: – If the bank normally charges 15% annual interest, that would’ve been around ₹2,500 extra for your iPhone over 6 months. But the merchant quietly pays that to the bank for you — so the EMI feels “free.” or in other ways your cost is somehow inflated to an extent that covers up for the free interest part !

Rimmi: Ohhh. Like a hidden sponsor in the background. Kind of like my dad when I first got my OTT subscription.

Gyan: Exactly! You enjoy the show; someone else handles the bill.

Rimmi: But why would the bank go for this? What’s in it for them if I’m not paying interest?

Gyan: Good question. Let me break it down:

Interest subsidy from the merchant – in your case, ₹2,500.

Interchange fee – the bank earns 1.5–2.5% from the store, say ₹1,200

You’re now locked in with that card for 6 months. Loyalty = future business.

Rimmi: Wow, they really planned this out. It’s like everyone’s making money off my excitement!

Gyan: True. And here’s the kicker — if you miss even one EMI payment? Boom. Late fees. Interest. Your “Zero Cost” EMI becomes “Mega Cost” EMI.

Rimmi: Okay okay, lesson learned! No late payments.

Gyan: And it’s not just phones. This happens with TVs, refrigerators, even fancy mattresses.

Rimmi: Mattresses?! So I could be paying for sleep… on EMI?

Gyan: Yup. Imagine paying ₹2,000 a month for 12 months — for a bed. That’s ₹24,000. But the bank gets a hidden ₹3,000 from the brand, and you sleep happy thinking you won the deal.

Rimmi: This is blowing my mind. So in a way, I’m part of a giant retail-finance conspiracy!

Gyan: Haha, not a conspiracy — just capitalism wrapped in a bow. But to be fair, if you’re financially disciplined, Zero Cost EMI can genuinely help spread out big purchases without strain.

Rimmi: As long as I don’t miss a payment or get carried away.

Gyan: Exactly. Use it smartly — like fire: great for cooking, dangerous if you don’t respect it.

Rimmi: Alright then, next stop: a new fridge on Zero Cost EMI — responsibly, of course. 😉